The CEE edition of PwC’s Voice of the Consumer Survey shows consumers in the region in 2024 carefully consider finances in retail choices and are willing to embrace new technologies and engage through social media channels.

In response, retailers and brands should consider how they best attain and retain customer trust in challenging times. They must meet consumer expectations of value while managing price increases to meet customer concerns about finances head-on. Retailers must incorporate and experiment with AI tools carefully, maintaining a human element and guarding personal data closely. They must also strike a balance in social media use for sales and engagement while being mindful of consumer concerns about its credibility.

The Global Voice of the Consumer Survey draws on insights amassed from 15 years of experience in consumer research—and collected the perspectives of more than 20,000 consumers across 31 countries and territories, including approaching 1,700 consumers from six CEE countries. Respondents expressed their views on a wide range of issues encompassing—the environment, health, data sharing and protection, value for money and embracing new technologies such as AI.

“This year's edition of the Voice of Consumer report is particularly crucial because a lot has happened over the last year—including the area of changes in consumer preferences: consumers returning to pre-pandemic habits, as well as checking new solutions, tools often supported by artificial intelligence, the use of which in business and private life aroused curiosity, hopes and fears at the same time. We asked consumers all around the world about their habits and preferences and would like to share a selection of conclusions that, in our opinion, define the modern consumer, their ambitions, prospects and key areas of uncertainty. This is the first time ever we completed the survey on a Central and Eastern Europe level, presenting typical habits and tendencies of a CEE consumer compared to a regular consumer of the world. We invite you to read the Voice of the Consumer 2024 report.”

Higher expected spendings in every retail category

Consumers across Central and Eastern Europe are bracing themselves for increased expenditures in various categories over the next six months. Foremost among those categories are groceries, clothing, travel, health and beauty and electronic devices. The pattern of increased spending in every category aligns with global consumer spending predictions but with regional nuances.

Thinking about your spending over the next 6 months, please choose, to the best of your ability, your expectations on spending in the following categories. (Aggregated answers)

In light of the European Green Deal’s stringent mandates on food quality and sustainable production, the grocery sector is projected to encounter the highest spending levels to date. These regulations are instrumental in propelling grocery prices upward—a trend that is further exacerbated by the significant inflation rates witnessed in the region over the past years. The CEE region faces additional challenges due to the uncertainty of Ukrainian grain exports, which have been disrupted since the Russian full-scale invasion in February 2022.

Central and Eastern European nations consistently display some of the highest inflation rates in the European Union. However, these countries are also experiencing rapid economic growth, which sets them apart from many other European nations. This vigorous growth is fostering expectations of rising incomes among CEE residents, leading to an increase in purchasing power and, consequently, consumer spending.

Despite inflation significantly decreasing in all surveyed countries, the share of consumers with anxiety regarding its future impact is still extraordinarily high (68%). This is marginally more than the almost two-thirds (64%) of consumers who cite inflation within their top three concerns in the Global Voice of the Consumer report. The recent rise in spending on non-essential items, however, suggests that consumer concerns about inflation may be easing. Inflation has eased substantially over the last year in all of the CEE countries included in the Voice of the Consumer Survey—Czechia: 14.3% to 3.1%, Hungary: 24.4% to 3.6%, Poland: 14% to 3%, Romania: 10.4% to 6.2%, Slovakia: 14% to 2.4% and Ukraine: 15.5 to 3.2%.

However, while concerns about inflation clearly remain, inflationary pressures are not as prevalent in Central and European economies as they were a year ago. The macroeconomic environment is also showing positive signs, with increases in wages and savings and greater credit availability. These factors are strengthening financial safeguards and enabling individuals to maintain a high quality of life despite economic challenges—which also indicates that households are successfully keeping up with, or even outpacing inflationary trends.

Year-on-year GDP growth

Source: https://www.imf.org/external/datamapper/profile/WEOWORLD

The observed increase in consumer spending across all categories is a multifaceted indicator of economic behaviour. It signifies not only a recovery in consumer confidence but also suggests that the purchasing power of households has remained resilient or strengthened in the face of inflationary pressures. This uptrend in expenditure is reflective of an economy where consumers are willing to allocate funds not just towards necessities like groceries but also towards enhancing their lifestyle and wellbeing by a positive increase in spending on luxury and other non-essential goods.

“Consumer sentiment is stabilising after a turbulent three years marked by pandemics, war, and inflationary situation. This is confirmed by the Consumer Confidence Index reaching its highest level since 2021. This encourages and allows many brands and merchants to be bolder in their marketing and sales efforts. In implementing them, it is worth keeping abreast of phenomena such as Smart Shopping, Compressed Commerce and Ad-driven Buying, as diagnosed by Allegro and Minds & Roses in their recent "Customer Journey 2024" study about shopping paths.”

Finances, health and seasonal food are key for CEE consumers

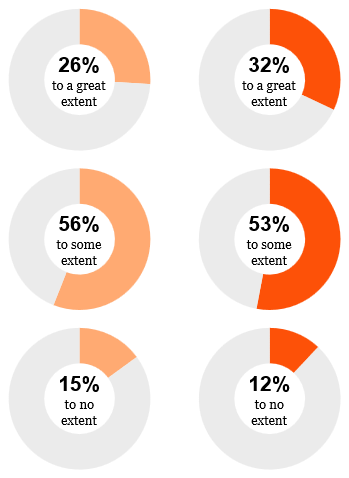

There are broad similarities between global and CEE consumers in their motivations for their food and dietary choices. In common with global averages, consumer behaviour in the CEE region countries surveyed, particularly emphasises the prioritisation of financial factors and health when it comes to dietary choices. Perhaps linked to the above section on inflation, financial choices loom largest for consumers in the CEE countries surveyed when purchasing food—with 11% more thinking about finances than global averages.

Which of the following do you consider when making food and dietary choices? (Ranked top 3)

The focus on finance is particularly starkly illustrated in Hungary and Slovakia, where a significant majority of consumers—75% and 74% respectively—consider the cost of products as one of the top three factors influencing their dietary decisions. This is a noteworthy deviation from patterns observed globally, where the financial aspect is just over half (52%).

The predominance of financial considerations in the CEE region can be attributed to the high inflation rates experienced between 2021 and 2023, which significantly and negatively influenced the purchasing power of consumers. As a result, financial constraints become a critical factor in decision-making processes, especially regarding essential items such as groceries.

Similar numbers of consumers globally (57%) and in the CEE countries surveyed (53%) cited general health as a significant motivator for food retail choices. CEE responses, however, show consumers are over one-tenth (11%) less likely to see nutritional information as a key determinant of how they do their grocery shopping.

Another significant difference is also visible in how many consumers in CEE value food being ‘in season’ when making purchasing choices. Local responses show CEE consumers are 10% more likely than consumers globally to seek out seasonal produce. This preference can perhaps be explained by the considerable proportion of agriculture in some CEE countries, by cultural aspects such as a strong preference of parts of the society for local cuisine based on seasonal vegetables or even by environmental consumer concerns. Importantly, seasonal local vegetables and fruit are also significantly cheaper when there is an abundance of them.

Overall, the focus on cost has important implications for CEE retailers who must navigate conflicting priorities in economies with rising prices. Grocery retailers have to carry out something of a balancing act—meeting customers’ expectations of value while simultaneously managing price increases effectively.

“Our objective here is not to fight the substitutes but rather to offer our customers the best value for money. We take deep dives into the needs of our customers and offer a carefully curated portfolio of own-label products across multiple pricing segments. We control the quality of these products and set competitive pricing. Our own-label products currently span three pricing segments—economy, mid-range and upscale—and represent over 24% of our total product range.”

Digital integration and in-store value

In Central and Eastern Europe, the adoption of various shopping channels is evolving, reflecting a blend of traditional and digital preferences. While the global trend leans heavily towards integrated digital platforms that combine social interaction with e-commerce, such as live commerce and community group buying, CEE consumers maintain a balance between online and in-store experiences.

In the last 12 months, how often have you bought products (e.g. clothes, books, electronics) using the following shopping channels? (Aggregated values)

When compared to global results, consumers in the CEE region shop less frequently in physical stores. This is a result of differences in grocery shopping habits and specifics of the structure of the grocery market such as different preferred store formats, different preferences for payment methods, varying penetration rates of the e-grocery market and consumers’ attitude towards delivery of groceries. Although consumers in CEE and globally show similar results of daily purchases from physical stores, the number of people who shop offline at least once a month is actually higher globally.

“The retail industry is constantly changing. In recent years, our customers used to buy mainly in big shopping centres, but now things are changing and the focus is moving also towards the smaller format. Proximity to the store became much more important to them. Another change has to do with local products. Our customers really appreciate Romanian products in the stores and we work with more than 700 partners who produce ultra-fresh products for the Carrefour chain. Another aspect we are focusing on is digitalisation, especially after this COVID period, when we have shifted a little bit from in-store shopping to online, so that we can serve customers through all channels.”

In the digital commerce landscape, mobile phones and personal computers are the preferred platforms for consumer purchases globally and in CEE, with a slight inclination towards mobile usage. However, the frequency of use for these online channels on a daily, weekly or monthly basis in the CEE region is lower when compared to the global average.

CEE consumers tend to exhibit modern shopping behaviours and proficiently navigate between traditional and online sales channels. This versatility enhances their capacity to access comprehensive product information and facilitates more informed purchasing decisions.

Thinking about when you shop for this category, which of the following channels, if any, do you anticipate using in a specific phase?

Showing an average across ten product categories: Electronic devices; Household appliances; Clothing and Footwear; Books, music, movies and video games; Furniture and homeware; Sports and outdoor equipment; Do-it-yourself/home improvement; Groceries; Toys; Health and beauty

The consumer journey in purchasing products typically unfolds in three key phases—discovery, research, and the final purchase. In the initial discovery phase of the purchasing process, potential consumers come across a product by physically browsing store aisles, through recommendations from friends and family, through digital channels and so on.

The subsequent research phase is crucial as consumers delve into details to inform their purchasing decisions. In the CEE region, this phase is predominantly conducted through online channels, with search engines like Google playing a pivotal role.

The final phase, the purchase, is most commonly completed in-store, reflecting the blend of traditional and modern shopping habits in CEE. Notably, approximately half of consumers in CEE prefer this traditional method of purchase, which parallels the global consumer pattern. This mix of behaviours confirms that CEE consumers are receptive to new technologies but may experience gradual adoption of novel purchasing methods.

“The online market is growing, and it is affected by external factors (shelling, air raids, destruction, etc.), and the buyer has become more picky about prices. Another important reason for choosing an online player is the corporate social responsibility of the store and its unfailing support for initiatives that are important for the country.”

As digital infrastructure improves and consumer behaviours evolve, it is projected that Central and Eastern Europe retailers will increasingly adopt digital shopping channels. To align with these changing consumer preferences, businesses should adopt a hybrid retail approach. This strategy should integrate the efficiency of digital channels while preserving the personalised experience offered by traditional in-store interactions. Such a balanced retail model is essential for businesses aiming to remain competitive and responsive to the dynamic retail landscape.

In terms of embracing new technologies, the CEE market demonstrates a more conservative approach. The adoption rates for innovative solutions such as smart home devices, wearables, and virtual reality (VR) are notably lower.

CEE consumers are open to using AI while also maintaining the human element

Consumer trust in artificial intelligence varies. There is, however, a general sense of optimism about the benefits of AI, as well as concerns about potential risks.

Consumers in CEE highly value the human element when getting recommendations on products or when they need to consult someone to acquire information they consider important. On the other hand, they are comfortable using AI for lower-risk activities like collating product information before purchase or handling basic customer service.

With further development of regulations around AI and continuous consumers’ demand for transparent and explainable AI instead of “black boxes” coupled with wider personal use of generative AI tools, the trust in AI is expected to grow. The future of building trust in AI hinges on responsible development, transparency, and ethical practices. As AI continues to evolve, organisations must prioritise user-centric approaches, foster collaboration, and proactively address consumer concerns.

Considering the recent advancements in Artificial Intelligence (AI) technology, which of the following activities would you trust AI to do accurately in place of human interaction?

Fear of threats connected to the wider use of AI in the CEE region stands out, with 86% of customers at least somewhat concerned about the increased risk of being scammed when using AI. This is a noticeably higher value than the already high global average of 77%.

However, consumers in CEE are less worried about potential job losses due to evolving AI capabilities. This stems from the specifics of the labour market in the region. Many CEE economies are either highly agrarian economies (e.g. Ukraine) or focused on heavy industries such as mining and automotive (e.g. Poland, Czechia, Slovakia). When looking at the GDP composition, Poland has the highest share of the industrial sector in the EU, while Czechia and Slovakia are both in the top five as well.

How concerned, if at all, are you about the following potential outcomes of future development and capabilities of AI technology? (Aggregated results for ‘concerned’)

Many actions are being taken to mitigate the negative outcomes of the developments in AI. Consumers’ views on AI, therefore, have the potential to rapidly change in the coming years.

As AI becomes more sophisticated, there is greater potential for its misuse through criminal activity. AI advancements, however, can also mean better detection and prevention systems. AI can be trained to recognise fraudulent patterns and mitigate cyber risks. As many as 40% of companies in CEE plan to use GenAI for cyber defence in the next 12 months—according to CEE findings from the 2024 Global Digital Trust Insights Survey.

Automation and AI can lead to job displacement, but they also create new job opportunities in tech and other sectors. As PwC's AI Jobs Barometer 2024 shows, openings for jobs that require specialist AI skills have grown 3.5 times faster than openings for all jobs since 2012. Also, this recent report reveals that jobs that require AI skills come with a wage premium of up to 25% in some markets.

The focus is shifting towards reskilling and upskilling the workforce to adapt to new roles that AI and automation will bring. According to the CEE edition of PwC’s 27th Annual Global CEO Survey, 57% of CEOs in CEE agree that generative AI will require most of their workforce to develop new skills over the next three years.

The regulatory landscape for AI is also evolving. For instance, the European Union has proposed the AI Act, which aims to set global standards and a harmonised legal framework for AI, addressing high-risk AI systems and promoting innovation while mitigating risks. The AI Act was recently approved by the Council of the EU.

Businesses in the CEE region can adapt to the evolving consumer preferences towards AI by developing hybrid customer service models that combine AI efficiency with the human touch for complex issues. Transparency about AI operations and decision-making processes can demystify the technology, addressing fears of scams and building consumer trust. Finally, committing to ethical AI practices and respecting consumer privacy will strengthen trust in AI technologies, facilitating a harmonious integration into daily life and business operations across the CEE region.

Subscribing to change

If available, how likely are you on a scale of 0 to 5 to move into a subscription-based payment method in any of the following categories? (Mean values)

0 is not at all likely; 5 is very likely.

The subscription model should be looked at from two perspectives—the consumer and the seller. The subscription-based sales model presents numerous benefits for sellers. It facilitates more accurate demand forecasting, which translates to revenue, bolsters customer loyalty, and provides avenues for dynamic pricing strategies and upselling opportunities by introducing premium plan options.

Looking from a customer's perspective, a subscription is a commitment to consume a certain level of goods or services. The attitude towards subscription models in retail is nuanced. It is convenient and potentially customisable through different plans, and often, it is cheaper when compared to the value of the same products sold in a traditional way. Consumer attitudes can vary vastly based on product types, with some categories being more suited to the subscription model than others.

If available, how likely are you on a scale of 0 to 5 to move into a subscription-based payment method in any of the following categories? (Percentage of respondents who answered 4 or 5 in a given category)

Categories in which most CEE customers are willing to switch to a subscription-based model are grocery, health and beauty, and travel. The first two most likely stem from consumers’ predictable demand for these products and the convenience of a subscription-based solution. In the case of travel, consumers probably expect to get higher value offers in subscription-based plans or access to additional services such as personalised recommendations or comprehensive trip planning.

Across the CEE region, 35% of consumers are willing to switch to a subscription-based model for grocery shopping. This percentage, however, varies vastly among CEE countries. In Hungary and Slovakia, less than 30% of customers want a subscription-based plan, while in Poland and Ukraine, this percentage is 41% and 47% respectively. Overall, the country with the best attitude towards subscriptions in retail in CEE is Poland, with an average willingness to switch to subscriptions across all retail positions of 2.23 (scale 0–5).

In Central and Eastern Europe, customer preferences for subscription services are influenced by a mix of cultural, economic, and market-specific factors, including the maturity of the market and the level of development of the payment infrastructure.

Navigating the green shift

What actions or behaviours, if any, have you taken to reduce your impact on climate change?

Thinking about the last 12 months, to what extent have you noticed climate-related disruption (e.g. more extreme temperatures, floods, storms, wildfire) in your day-to-day living?

Consumers in CEE are well aware of climate disruptions, and 87% of them claim to take action to reduce their personal impact on climate change. As many as 43% of consumers in CEE are making more considered purchases with the aim of reducing their overall consumption. Also, 39% are buying more sustainable products or products with a reduced climate impact.

What is more, some CEE consumers claim they are willing to pay more for sustainably produced or sourced goods. For example, 24% of them say they are willing to pay 1-5% more for products that are produced/sourced locally, 27% would pay 6-10% more, 18%—11-20% more, 8%—21-30% more and 8% of CEE consumers are ready to pay more than 30% sustainability premium in this category.

However, looking at questions that are not climate or environment-oriented, we see a different picture. In questions about potential threats and risks that could impact customers’ country, factors that could reduce the number of returns customers make, enticements for brand switching and food and dietary choices, we see that customers tend to put ecological motivation lower than others, in particular financial factors.

Many EU regulations regarding recycling and ESG reporting are being introduced—and it also may influence consumer attitudes towards sustainability. Implementation of the Corporate Sustainability Reporting Directive (CSRD) will require large companies to publish reports on measures taken to mitigate climate risks in 2025. Additionally, the EU countries are introducing deposit-refund systems (DRS) to meet the requirement to achieve certain levels of recycling rates by 2029.

As a result, the topic of sustainability will be brought closer to the consumer, and more data will become available to analyse the performance of companies in the ESG matter. This trend, coupled with the greater care for the environment among younger generations, indicates that businesses, particularly in the retail sector, must prioritise environmentally responsible practices to attract and retain customers.

About the Survey

In January and February 2024, PwC surveyed 20,662 consumers across 31 countries and territories. Six CEE countries which were part of the survey—the Czech Republic, Hungary, Poland, Romania, Slovakia and Ukraine— collected 1,681 responses. The representative sample size allowed for statistically significant conclusions and comparisons of consumer trends between individual countries, regional level and the global results. The respondents were at least 18 years old and were asked about a range of topics relating to consumer trends, including shopping behaviours, emerging technology and social media.

Interviews with industry executives included in localised versions of this report took place in May 2024.

Note: due to rounding, not all reported percentages may equal 100%.

Contact us